When applying for a home loan in India, a borrower’s credit score is one of the most important factors determining his/her eligibility and interest rates. Financial institutions can offer discounts of 10 to 100 basis points (bps) to loan applicants with credit scores of 750+, where 1 bps is equal to 1/100th percentage.

A credit score is a 3-digit number that tells the lender how an applicant has behaved as a borrower and his/her repayment habits. In India, the credit score given by Credit Bureau TransUnion CIBIL carries the highest weightage.

The following sections will explain the meaning of CIBIL score, its importance and what counts as a good score.

Understanding the meaning of CIBIL score

The Credit Information Bureau India Limited (CIBIL) is one of the most esteemed companies that provide credit scores. Along with Experian, Equifax and Highmark, CIBIL is one of 4 credit bureaus authorised by RBI to keep credit records. Of these, CIBIL is the country’s first and most important credit agency.

Most financial institutions in India prefer CIBIL scores over other credit scores as they have tie-ups with it. CIBIL score is a 3-digit score between 300 to 900, where 300 is the worst score while 900 is the highest. When applying for home loan, one must maintain a CIBIL score of at least 750 for the best terms.

The CIBIL score assesses an individual’s creditworthiness based on his/her credit history, repayment habits, ongoing liabilities, pending loan applications, etc. It results from complex calculations based on information from one’s credit history as recorded in CIBIL’s database. This information is present in a loan applicant’s Credit Information Report (CIR).

Significance of the CIBIL score

The following points describe the importance of a CIBIL score:

-

Determines an individual’s credit behaviour

CIBIL score gives an insight into how a person managed his/her credit in the past. Lenders can use this to check an applicant’s credit card usage, credit utilisation ratio and repayments on previous/current loans.

-

Helps to understand one’s repayment capacity

When someone applies for a home loan in India, the lender checks his/her CIBIL score to determine his/her repayment capacity. One’s monthly income and CIBIL score help lenders decide if he/she repay his/her loan on time.

-

Determine eligibility

Having a good CIBIL score (around 750) is a necessary home loan eligibility criteria for a higher loan amount. With a lower CIBIL score, an applicant will have to settle a lower loan-to-value (LTV).

-

For better interest rates

A good CIBIL score makes one eligible for better home loan interest rates from a wide range of lenders. If one has a good CIBIL score, more financial institutions will want to offer him/her a home loan. This would enable him/her to choose to negotiate the best deal to read about forbes.

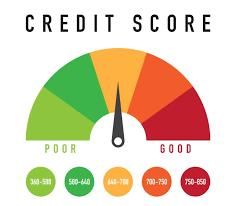

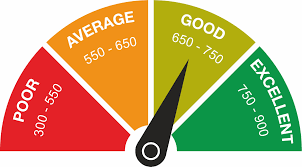

What is a good CIBIL score for a home loan?

One needs to check the following list of score ranges to find what a good CIBIL score is.

- N/A or Nil: This implies that a loan applicant does not have sufficient credit history. Financial institutions may hesitate to give someone without a credit score a loan.

- 300 – 549: Scores below 550 convey a poor CIBIL score and greatly reduces the chances of getting a loan. Financial institutions may agree to offer lower amounts at higher rates of interest or against collaterals.

- 550 – 649: CIBIL scores in the 550-649 range are average, and one needs to work on increasing it to secure a home loan. Applicants will have limited options with such scores and can get a loan with higher interest rates.

- 650 – 749: A score between this range is a good CIBIL score. Having a score above 650 is the minimum home loan eligibility criteria for competitive interest rates. However, this is not the best CIBIL score, and lenders consider other factors such as employment stability and monthly income before approving a loan.

- Above 750: Chances of loan approval with excellent CIBIL scores are extremely high. Furthermore, applicants will be in a position to negotiate for the best home loan interest rates and amounts with several lenders.

Tips to improve one’s CIBIL scores

One can follow the given tips to improve his/her CIBIL scores:

- An applicant should pay off his/her outstanding debts before applying for a home loan.

- If one has many credit cards with low balances, he/she should pay them off or transfer them to one card.

- It is a good idea to limit the use of one’s credit limit to around 30% to improve his/her CIBIL score.

- Loan applicants can build their CIBIL score over time by paying EMIs and credit card debt on time. However, they must not default on their EMIs or make late payments.

- One should regularly check his/her CIBIL score to make sure that there are no errors or omissions.

With an improved CIBIL score, individuals can easily qualify for a housing loan. However, to help with the application process, financial institutions have introduced pre-approved offers. These offers are available on financial products like home loans, LAPs, etc., and help to streamline a loan application and save time. Borrowers can check their pre-approved offers by submitting their essential contact details to learn about komo news.

To sum up, understanding the meaning of CIBIL score and what constitutes a poor, average, good or excellent CIBIL score is imperative. It helps borrowers to prepare and apply for a loan accordingly and avoid facing rejection.

Download apps from tweakvip and tweakvip

Go to homepage